German components distribution: slight sales growth in 2023, negative outlook for 2024

-

- Tweet

- Pin It

- Condividi per email

-

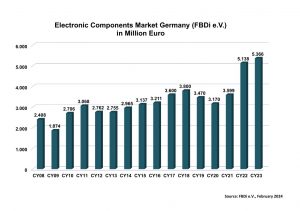

In the fourth quarter, the weak order intake of the last few quarters clearly hit sales. The turnover of FBDi‘s registered distributors fell by 20.1% to 1.08 billion Euros. As a result of the continued very weak bookings situation (-56% to 507 million Euros), the book-to-bill ratio ended at 0.47, indicating a difficult market situation for the coming quarters. Nevertheless, the full year 2023 remained positive despite the weak second half. Total revenues closed with an increase of 4.4% to 5.37 billion Euros.

The year for distributors was dominated by semiconductors. Although sales in the fourth quarter also fell by 21% to €745 million, for the year as a whole they grew by more than 10% to a record €3.73 billion. Passive components and Electromechanics performed less well (and have been doing so for some time). They shrank both in the fourth quarter and for the year as a whole, with Passives down 15.9% to 136 million Euros in the fourth quarter (full year: -5.6% to 669 million Euros) and Electromechanics down 18.1% to 128 million Euros (full year: -7.3% to 620 million Euros). Similar declines were recorded for sensors, displays, power supplies and assemblies. The distribution of sales by component group remained almost unchanged.

FBDi CEO Georg Steinberger: “The figures are not surprising, neither for the fourth quarter nor for the year as a whole. 2023 can be summarized by saying that it already includes a lot of business brought forward from 2024 and was therefore unrealistically high, which is exactly what will be missing in 2024. The next few quarters are likely to see a low level of new orders in the existing business, so the focus should clearly be on developing new designs and projects, which have probably not been a priority for customers due to the difficult delivery situation over the last two years.”

Looking ahead, Steinberger said: “The positive outlook of most market researchers for 2024 mainly concerns one area that could serve as a driver – memory and processors that support AI applications in data centers. This market is likely to be driven mainly by the US. The reality in Europe is different: We are facing a weakening industrial sector and an automotive sector under pressure, which are the two main customers for components and the main customer groups for distribution. The outlook for Europe this year is therefore rather moderate, with the hope of a turnaround after the summer. Our appeal would be not to get involved in pointless price wars, especially as component production costs are not getting any lower, but to focus on Europe’s innovative strength and inspire the market with new ideas”.

News/Analysis read all ▶

-

KYOCERA AVX launches new solderless WTB card-edge connectors

KYOCERA AVX launches new solderless WTB card-edge connectorsKYOCERA AVX launched the new 9169-000 Series single-piece wire-to-board card-edge connectors. The new 9169-000...

-

Renesas completes acquisition of Transphorm

Renesas completes acquisition of TransphormRenesas Electronics Corporation announced that it has completed the acquisition of Transphorm. With the...

-

Linxens and Nocturnal join forces to accelerate the development of innovative medical devices

Linxens and Nocturnal join forces to accelerate the development of innovative medical devicesLinxens, global expert in the design and manufacture of electronic components, and Nocturnal, specialized...

Products read all ▶

-

Advantech launches ITA-168/178 series

Advantech launches ITA-168/178 seriesAdvantech launches its latest compact and fanless edge computers—the ITA-168 and 178 series. These...

-

Solid Sands launches SuperGuard Amsterdam version 1.2

Solid Sands launches SuperGuard Amsterdam version 1.2Solid Sands has launched an updated version of its SuperGuard product, the world’s first...

-

A new add-on board for global tracking and telematics from MIKROE

A new add-on board for global tracking and telematics from MIKROEMIKROE has launched 4G LTE&GNSS Click, a compact add-on board designed for advanced global...

{kind=link}